Why Choose BizCare?

Employees are individuals, so why should their health insurance be one-size-fits-all? BizCare provides a personalized and flexible approach, giving employees more options than traditional group health insurance while enabling companies to deliver equivalent coverage, often at a lower cost.

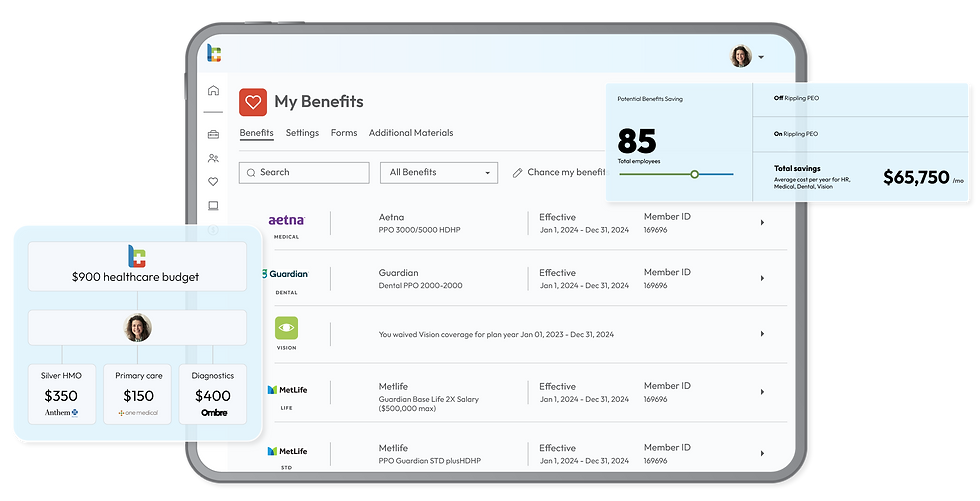

Flexible Healthcare Options

Traditional group health insurance limits employees to just a few plan choices, but BizCare's innovative ICHRA solution offers them hundreds of options through the ACA marketplace, meaning individuals can find the plan that best fits their needs.

Maximize Savings

Opt for an ICHRA-based health solution to save money by eliminating broker fees, paying only for employees who utilize the plan, sidestepping annual premium hikes through a fixed reimbursement amount, and accessing large group health plans for less.

On-Demand Experts

Our team removes the administrative burden on your HR department while providing a personalized enrollment process and continued support for everyone.

Available to All Employees

Traditional group health plans restrict assistance to full-time employees. However, you can now offer varying reimbursement amounts based on employee classification, ensuring all your employees can access the health coverage they need.

Easily Stay Compliant

BizCare handles your company's ACA and COBRA compliance, ensuring every aspect is covered. We monitor federal, state, and local regulations, providing peace of mind that your workplace consistently meets all standards.

Switch Plans Anytime

Switching plans is no longer limited to once a year or tied to a qualifying event. ICHRAs enable individuals to change plans whenever needed—because life moves quickly, and health insurance should too.

What is an ICHRA?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is a type of health benefit that allows employers to reimburse employees tax-free for individual health insurance premiums and qualified medical expenses.

ICHRAs offer the entirety of the ACA marketplace for plan selection

ICHAs satisfy the Affordable Care Act employer mandate

ICHRAs can be offered instead of or in addition to traditional group health plans

ICHRAs allow employers to set their own reimbursement amount

20M+

People have enrolled in individual insurance plans on the ACA Marketplace

81%

Of employers face a renewal cost hike each year that can be mitigated with an ICHRA

16%

Is the average amount of money saved by moving from a traditional group plan to an ICHRA

ICHRAs by the Numbers

H1 Heading

H2 Heading 54

H3 Heading 46

H4 Heading 37

H5 Heading 27

H6 Heading

Paragraph 1 Heading 27

Paragraph 2 Heading 22

Paragraph 3 Heading 18

ICHRA vs Traditional Group Plans

Here's a subheadline if needed

.png)

Health Benefits for Businesses Big and Small

From 10 employees to 10,000, BizCare has a health benefits solution that’s perfect for your company.

1

Adopt

Employer defines contributions and open enrollment

2

Enroll

Employee shops & buys coverage with a unique account number

3

Manage

Employer receives consolidated monthly statement

4

Pay

Insurers are happy because they get paid on time every time

How It Works

Partnered with Leading Insurance Companies

Could BizCare and your company form the ideal partnership? Contact us by phone or the form below and let's explore the possibilities together.

Hear from Our Customers

״Use this space to share a testimonial quote about the business, its products or its services. Insert a quote from a real customer or client here to build trust and win over site visitors.״

— Jane Clarke

״Use this space to share a testimonial quote about the business, its products or its services. Insert a quote from a real customer or client here to build trust and win over site visitors.״

— Michelle Knight

״Use this space to share a testimonial quote about the business, its products or its services. Insert a quote from a real customer or client here to build trust and win over site visitors.״

— Ben Preston

Get in Touch

You're probably

wondering...

-

How do ICHRAs provide employers with greater control over their health benefit budgets compared to traditional group plans?Unlike some group plans, ICHRAs allow employers to set their own budget without minimum contribution levels.

-

How do ICHRAs enable employers to extend health benefits to employee classes that are typically ineligible under traditional group plans?ICHRAs can be used to provide health benefits to employee classes that may not have been eligible under traditional group plans

-

How can employers potentially reduce costs while offering comparable coverage through ICHRAs?By leveraging the larger risk pool of the individual insurance market, employers may be able to offer comparable coverage at a lower cost.

-

How do ICHRAs offer scalability and flexibility for businesses experiencing growth or fluctuations in their workforce size?ICHRAs can be easily scaled as a company grows, making them particularly attractive for businesses anticipating expansion or those with fluctuating workforce sizes.

-

How do Individual Coverage Health Reimbursement Arrangements (ICHRAs) provide flexibility in tailoring benefits for different employee classes?ICHRAs allow employers to offer different allowances based on employee classes (e.g. full-time vs part-time), providing more flexibility in tailoring benefits.

-

How does accessing the individual market through ICHRAs benefit employees in terms of network options and coverage comprehensiveness compared to a single group plan?By accessing the individual market, employees might find plans with broader networks or more comprehensive coverage than what a single group plan could offer.

-

How do ICHRAs enable employers to tailor benefit levels for different classes of employees, such as full-time, part-time, and seasonal workers?Employers can offer varying benefit levels to different classes of employees (e.g., full-time, part-time, seasonal), allowing for more tailored benefits strategies.

-

How do ICHRAs assist employers in meeting Affordable Care Act (ACA) requirements while reducing the complexities and compliance risks associated with managing a group health plan?ICHRAs can help employers meet Affordable Care Act (ACA) requirements without the complexities of managing a group health plan, potentially reducing compliance risks.

-

How do ICHRAs simplify health benefit administration for employers?Employers can avoid the complexities of managing a group health plan while still providing health benefits.

-

How do ICHRAs offer flexibility in terms of implementation timing for employers transitioning from group plans or starting to offer health benefits?ICHRAs can be implemented at any time during the year, providing flexibility for employers to transition from group plans or start offering health benefits when it best suits their business needs.

-

What are the tax benefits of ICHRAs for both employers and employees?ICHRA contributions are tax-deductible for employers and free of payroll taxes. Reimbursements are also tax-free for employees.

-

How do the flexibility and personalization of ICHRAs enhance their attractiveness to current and prospective employees?The flexibility and personalization of ICHRAs can be an attractive benefit for current and prospective employees.

-

How do ICHRAs empower employees to choose health insurance coverage that better suits their individual needs?Employees can select individual health insurance plans that best fit their unique needs, rather than being limited to a one-size-fits-all group plan.

-

How does an Individual Coverage Health Reimbursement Arrangement (ICHRA) help employers manage healthcare spending more effectively?With an ICHRA, employers can set a defined contribution amount for each employee, giving them more control and predictability over healthcare spending compared to the often unpredictable and rising costs of traditional group plans.

-

How can ICHRAs be integrated with other benefit offerings like Direct Primary Care (DPC) to enhance the overall benefits package for employees?ICHRAs can be combined with other benefit offerings, such as Direct Primary Care (DPC), to create a more comprehensive and attractive benefits package

-

How do ICHRAs benefit companies with employees who have alternative coverage options by not requiring a minimum participation percentage?Unlike group plans, ICHRAs don't require a minimum percentage of employees to participate, which can be beneficial for companies with employees who may have coverage through other sources.